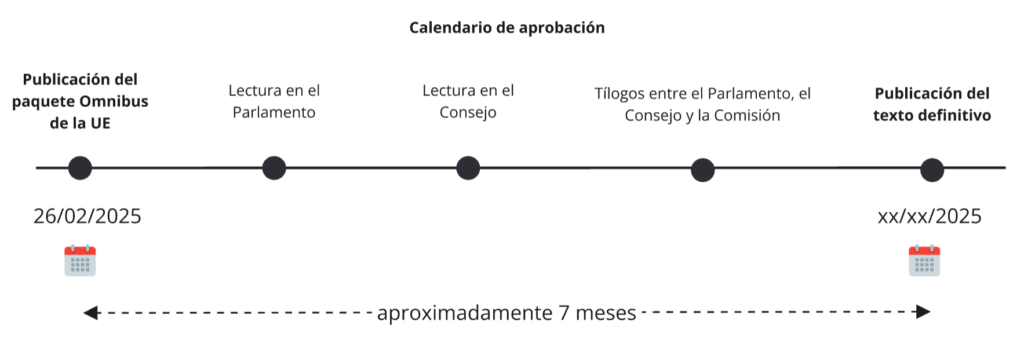

On 26 February 2025, the first Omnibus package was unveiled, consisting of a series of proposed Directives and Regulations aimed at simplifying and harmonising different regulations. These amendments have a direct impact on the Corporate Sustainability Reporting Directive (CSRD), the Corporate Sustainability Due Diligence Directive (CSDDD), the EU Taxonomy and the Carbon-Boundary Adjustment Mechanism (CBAM).

In this article we review the main proposals for amending the CSRD.

Companies affected

Initially, the CSRD applied to:

- Large companies and group parent companies that are public interest entities with more than 500 employees.

- Large companies and group parents not considered to be in the public interest, but subject to the same reporting criteria.

- Listed SMEs, except for micro-enterprises, which had to comply with specific disclosure requirements.

With the amendments introduced in the Omnibus Package, the threshold for a company to be considered as affected by the CSRD is extended. The directive will now apply to large companies with more than 1,000 employees and which meet at least one of the following financial criteria:

- Turnover in excess of 50 million euros.

- A total balance of more than 25 million euros.

This adjustment excludes those smaller ones that were initially required to report.

Timetable for implementation

The CSRD entered into force on 1 January 2024. The Omnibus package proposes to postpone the reporting requirements by two years. For companies for which it applies in 2025, the implementation date will be 2027 and for companies for which it applies in 2026, the implementation date will be 2028.

This delay aims to give companies more time to adapt their data collection and verification systems, ensuring a more orderly transition to the new sustainability framework.

European Sustainability Reporting Standards (ESRS)

The CSRD requires companies to use the European Sustainability Reporting Standards (ESRS).

The Omnibus package introduces a revision of the ESRS with the aim of:

- Reduce the reporting burden by eliminating redundant or irrelevant metrics.

- Clarify the content, providing greater precision in indicators and methodologies.

- Improve consistency by aligning standards with international frameworks such as ISSB and GRI.

Sectoral ESRS

Originally, it was planned to develop sector-specific ESRS for nine sectors with detailed industry-specific requirements. However, the Omnibus package states that no sector-specific ESRS will be developed at this stage, prioritising the implementation of general standards before addressing more specific regulations.

SMEs and their inclusion in the CSRD

Under the original regulation, listed SMEs are obliged to report from 2027. However, the Omnibus package proposes to withdraw this obligation.

Verification of reported information

The CSRD envisages a progressive process of auditing sustainability reports, with the transition from limited verification to reasonable verification from 2028.

However, the Omnibus package proposes to remove the requirement to move from limited to reasonable verification, allowing companies to maintain a more flexible approach to auditing their sustainability reporting.